Market & Portfolio Update

Q4 2025

Prepared by the Investment Management Committee – January 2026

This report is provided for information purposes only and does not constitute personal investment advice. The content reflects Welsh & Taylor Wealth’s views as at January 2026 and may change without notice.

Market Overview

Overall, Q4 2025 was a steady quarter for global markets, with most major indices posting modest gains as investors became more confident that interest rates are likely to be cut by central banks in 2026. Generally, lower interest rates mean higher returns for risk assets like stocks and gold. Inflation continued easing in the US, UK and Europe, and corporate earnings held up better than expected.

At the same time, a surprising geopolitical story dominated headlines - the ongoing tensions around President Trump’s attempt to assert control over Greenland, which led to tariff threats and strong pushback from Europe. Although dramatic, these events caused far less disruption to markets than the headlines suggested, and markets largely took the noise in their stride however the market has sold off from its record highs.

Global markets remained resilient overall, and finished the year on a very positive note. Even with periods of volatility, 2025 was a good year to be an investor.

Why Markets Remain Strong

Below is a simple summary of how the major markets performed in Q4 2025:

-

The S&P 500 gained 2.2% over the quarter, helped by expectations of 2026 rate cuts and stronger‑than‑expected corporate earnings. Tech stocks were steadier after earlier strong gains, but overall the US market continued to show resilience. The S&P 500 closed the year +15.96%.

-

UK equities outperformed the US in Q4, with the FTSE 100 rising 5.3%, supported by easing inflation and a more stable interest‑rate outlook from the Bank of England. Since then the FTSE was able to close above 10,000 for the first time. The FTSE 100 closed the year +21%.

-

European markets delivered solid returns, with the Euro STOXX index up 4.4% in the quarter, helped by the expectation of 2026 rate cuts and improving investor sentiment. The Euro STOXX closed the year +20.9%.

-

Global equities (MSCI World) delivered a positive return of roughly 3% in Q4, rounding off a strong year for global markets overall. The MSCI World index closed the year +19.03%.

In summary, most major markets delivered steady, positive returns, with Europe and the UK outperforming the US over the quarter - a reversal of the pattern seen in much of the last decade.

Trump-Greenland Overview

While the headlines around President Trump and Greenland may seem unusual, there are clear strategic reasons behind his push - reasons that help explain why this story dominated geopolitical news in Q4.

-

Trump has publicly argued that controlling Greenland would strengthen U.S. national security, particularly given its location between North America, Russia, and the Arctic shipping routes.

-

Trump has repeatedly claimed that if the U.S. didn’t take control of Greenland, it could fall under the influence of Russia or China - despite NATO allies disputing this narrative.

-

Greenland is rich in minerals and sits along emerging Arctic sea routes as ice continues to recede. These routes could become strategically and economically significant over the coming decades, something that has intensified global interest in the region. Several European countries have warned that Trump’s approach raises diplomatic and economic risks for the wider transatlantic relationship.

-

Some of the rhetoric around Greenland has been tied to political considerations. In one message to European leaders, Trump connected his hardening stance to feeling “no obligation to think purely of Peace” after not receiving the Nobel Prize, further escalating tensions and bringing military threats and new tariffs into play.

The key message remains the same - short‑term events, political or economic, are unpredictable. What matters is staying diversified, disciplined, and focused on long‑term goals.

Q4 once again showed that:

Markets can perform well even during political noise.

Earnings and economic fundamentals matter more than headlines.

Diversification across regions (US, UK, Europe, global) continues to be the most effective long‑term approach.

Portfolio Insights

Our Investment Committee regularly reviews portfolio positioning to ensure it remains aligned with market conditions, our long-term strategy, and the best interests of our clients.

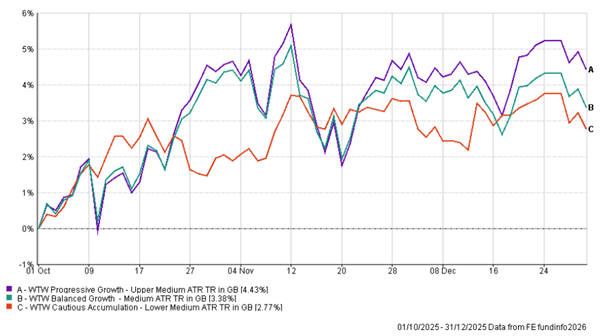

Below is a summary of performance for our three core WTW portfolios:

Q4 2025 Portfolio Performance (1 October 2025 – 31 December 2025)

Assessing Value and Client Outcomes

As part of our ongoing commitment to delivering good outcomes for clients, we regularly assess whether our portfolios continue to meet their stated objectives and represent fair value. This involves reviewing performance, cost efficiency, risk management, and suitability against client expectations and the broader market environment.

-

Risk Profile: Upper-Medium

Total Return: +4.43%

Sharpe Ratio: 1.18

Annual Fund Charge: 0.08%

WTW Progressive Growth Portfolio

Objective:

To generate long-term capital growth by providing broad exposure to global equity markets. With an allocation of 80–100% in equities, the portfolio seeks to benefit from growth opportunities across developed and emerging markets while maintaining diversification.Assessment:

The Progressive Growth Portfolio has achieved +4.43% in Q4 2025, driven by strong US equity exposure and contributions from global developed markets.The portfolio is performing in line with expectations for its risk level.

Returns have been achieved with controlled drawdowns and strong diversification.

Fees remain competitive compared to similar actively managed portfolios, supporting positive long-term value.

The Progressive Growth Portfolio is delivering on its goal of high-conviction, diversified global growth, and continues to represent fair value by balancing cost, performance, and risk effectively.

-

Risk Profile: Medium

Total Return: +3.38%

Sharpe Ratio: 1.24

Annual Fund Charge: 0.08%

Objective:

To provide long-term capital growth by investing across developed global markets. The portfolio balances growth opportunities with risk management, aiming to deliver strong returns over the medium to long term.Assessment:

In Q4 2025, the Balanced Growth Portfolio has returned +3.38%, reflecting strong global equity performance alongside well-managed fixed income exposure.The portfolio’s equity exposure has captured global market gains, particularly from US and developed world indices.

Diversified bond holdings have provided stability and income.

Risk-adjusted performance (Sharpe ratio of 1.35) indicates efficient returns relative to volatility.

The portfolio continues to offer fair value, achieving solid growth while keeping volatility at an appropriate level for investors with a balanced risk appetite.

-

Risk Profile: Lower Medium

Total Return: +2.77%

Sharpe Ratio: 1.13

Annual Fund Charge: 0.17%

Objective:

To achieve long-term growth while managing volatility through diversification across fixed interest, cash, commodities, and equities. This balanced approach allows access to growth markets while reducing exposure to the fluctuations of the overall stock market.Assessment:

The Cautious Portfolio has delivered +2.77% in Q4 2025, which we consider a positive outcome given its defensive positioning and low risk exposure. The portfolio has benefited from steady bond and money market performance, alongside modest equity growth and positive contributions from gold.Volatility remains low and within the portfolio’s target range.

Diversification is delivering as intended - smoothing returns through a mix of defensive and growth assets.

Ongoing charges remain competitive relative to the peer group, and the fund mix continues to prioritise liquidity and cost efficiency.

Overall, the portfolio is meeting its objective of steady growth with controlled risk, representing fair value for investors seeking capital preservation and gradual appreciation.

Summary:

Across all three portfolios, performance has been positive and risk levels are consistent with client expectations and the stated aims of each strategy. The combination of robust investment governance, transparent costs, and strong early performance indicates that the WTW portfolio range is delivering good outcomes and represents fair value for clients.

How Do Our Portfolios Compare?

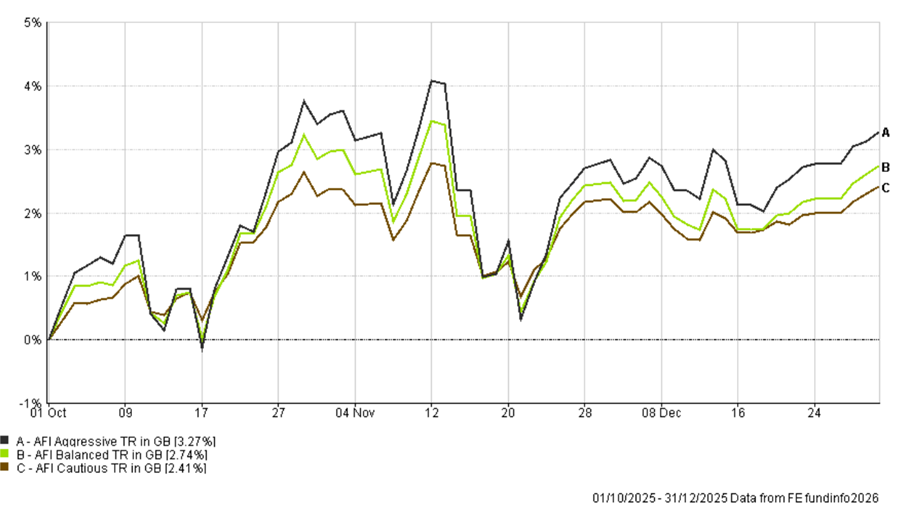

To assess performance objectively, we compare our portfolios against the Adviser Fund Index (AFI) - a recognised industry benchmark compiled by Financial Express from the recommended portfolios of leading UK financial advisers.

The AFI represents a realistic “market average” for professionally managed portfolios across three risk levels:

AFI Cautious - lower-risk portfolios with a higher allocation to bonds and cash.

AFI Balanced - medium-risk portfolios combining equities and fixed income for steady growth.

AFI Aggressive - higher-risk portfolios with greater exposure to global equities.

By comparing each WTW portfolio to its corresponding AFI benchmark, we can objectively determine whether our portfolios are providing clients with added value relative to the broader advice market.

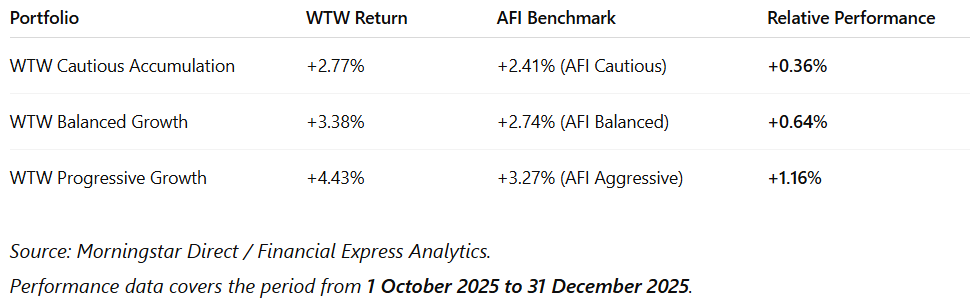

Performance Comparison (1 October 2025 - 31 December 2025)

Why Our Portfolios Have Outperformed

Our portfolios have delivered stronger returns than the AFI benchmarks primarily due to three key factors:

-

Many UK‑advised portfolios continue to hold a strong domestic bias, with heavy allocations to UK equities and gilts. While the UK performed well in Q4 2025, global markets - particularly the US and wider developed markets - continued to offer stronger long‑term risk‑adjusted opportunities.

Because our portfolios are built with broad global exposure, including the US, Europe, and worldwide developed markets, they benefited directly from:

Steady gains in the S&P 500

Stronger performance across European equities

A positive quarter for global indices like MSCI World

This global orientation helped lift returns relative to UK‑centric benchmarks and provided more stable participation across different regions.

-

Gold has been one of the standout assets in 2025, reaching record highs and delivering strong year‑to‑date returns. Our decision to include physical gold exposure via the Invesco ETC has been a significant driver of relative performance, especially because:

Gold prices have surged due to rising geopolitical tensions

Events such as President Trump’s escalating attempt to assert control over Greenland, combined with tariff threats and heightened transatlantic tensions, increased demand for safe‑haven assets. Investors typically turn to gold during periods when global politics feel less predictable, and this quarter was no exception.

Lower expected interest rates support gold

With major central banks shifting toward monetary easing and rate cuts expected in 2026, the backdrop for gold has been increasingly favourable. Lower interest rates reduce the opportunity cost of holding gold, helping support higher prices.

AFI benchmarks have little or no exposure to gold

This has created a meaningful gap. While the AFI composites miss out on the diversification and return benefit that gold has delivered, our portfolios - with a deliberate allocation - have captured both stability and upside.

Gold’s role is twofold:

It boosts returns during supportive environments like we’ve seen this year.

It provides ballast when equity markets wobble.

This dual benefit has been an important contributor to our outperformance.

-

We focus on institutional‑class passive funds and ETFs, which offer:

Lower ongoing costs

High liquidity

Transparent implementation

Lower costs mean clients keep more of their returns. High liquidity allows us to adjust allocations efficiently when needed, without friction.

This combination ensures that the portfolio captures market performance cleanly, with minimal fee drag - an advantage versus many peers within the AFI benchmark group, where fees and less‐efficient structures often erode returns.

Balancing Risk and Return

Importantly, all three of our portfolios have outperformed their respective AFI benchmarks without taking on more risk. This means clients benefited from more efficient portfolios - not riskier ones. Outperformance came from diversification, discipline, and intelligent asset allocation, rather than betting on any single region or theme.

Summary

Across the range, each WTW portfolio has delivered superior outcomes versus its AFI benchmark since launch. This supports our core investment philosophy - that disciplined global diversification, cost control, and thoughtful risk management lead to better client outcomes over time. We remain confident that this approach will continue to add value as markets evolve into 2026.

Outlook on Gold

Gold has been one of the most reliable defensive assets during periods of global tension, and the geopolitical backdrop - including events like the U.S.–Europe confrontation over Greenland - strengthens the case for maintaining our 10-15% portfolio allocation.

Why We Continue to Hold Gold:

-

Major geopolitical events, such as tariff threats, military posturing, or sudden shifts in international alliances, typically increase demand for gold as a safe‑haven asset. The ongoing tensions around Greenland - including threats of tariffs of up to 25% on multiple NATO allies and heated diplomatic exchanges - highlight why investors often turn to gold during periods of global instability.

-

With the U.S. Federal Reserve, Bank of England, and European Central Bank all expected to cut interest rates further in 2026, the outlook for gold remains favourable.

Lower interest rates reduce the “opportunity cost” of holding gold (since it doesn’t pay interest), historically supporting stronger prices. This aligns with the broader Q4 2025 environment, where expectations of monetary easing helped push gold to record highs throughout 2025. -

Global central banks continued buying gold at historically elevated levels throughout 2024 and 2025, reinforcing long‑term structural demand. While this wasn’t part of the Q4 2025 news flow, it remains a key factor that supports long‑term pricing and stability - and strengthens our conviction in holding physical gold exposure.

-

Gold behaves differently from equities and bonds. When markets wobble, whether due to political tension, interest‑rate uncertainty, or global economic shifts, gold has historically provided ballast. Retaining investment allocation to gold ensures our portfolios remain resilient across a wider range of scenarios, without relying on any single region or asset class.

Why We Are Not Making Any Changes at This Time

As we enter 2026, our message remains simple and consistent: we are not making any changes to the portfolios at this time. The portfolios continue to behave exactly as intended - balancing growth, risk, diversification, and liquidity in a disciplined and repeatable way.

-

Recent geopolitical tensions - most notably President Trump’s escalating attempt to push for control of Greenland, and the tariff threats this has triggered across Europe and NATO allies - have created short‑term uncertainty in headlines.

Europe has already held emergency meetings in response to these tariff threats, highlighting how sensitive the situation has become in the final weeks of the year. Trump has also warned of 10%–25% tariffs unless European nations agree to a deal on Greenland, increasing short‑term geopolitical volatility.

Events like this can cause short‑term market movements, but they rarely alter the long‑term trajectory of diversified portfolios. Acting hastily in the middle of such events would feel counterproductive, especially when:

Markets have remained resilient despite the noise, and

These geopolitical developments may shift again quickly, as they often do.

-

Our portfolios are designed with a clear philosophy: Focus on long‑term outcomes, not short‑term reactions.

We expect periods of volatility. We expect political surprises. We expect shifting narratives. What we do not expect, nor want, is to chase every headline.

Short‑term adjustments based on fast‑moving geopolitical stories risk doing more harm than good. Instead, we follow a strategy built on:

Global diversification

Discipline and consistency

Intelligent risk management

High‑quality, low‑cost implementation

This approach has been the driver of our strong risk‑adjusted performance through 2025.

-

We will continue to review market conditions as part of our regular investment governance process. However, we will only make changes when we believe they will genuinely improve long‑term client outcomes.

We continue to research lower‑cost and more efficient funds, but cost is only one part of the equation. Liquidity, transparency, and reliability matter just as much - especially during periods when the global backdrop feels uncertain.

Looking Ahead

The outlook as we enter 2026:

Interest rate cuts in the US, UK and Europe appear increasingly likely.

Inflation continues to cool.

Corporate earnings remain supportive.

Geopolitics, including the US election cycle and the Greenland dispute, will create noise but should not drive long‑term decisions.

We will continue to monitor global developments closely and adjust portfolios only when it is in clients’ long‑term interests.

While we are not making any portfolio changes at this time, we are continuously reviewing opportunities that could strengthen long‑term client outcomes. Our investment process is deliberately forward‑looking, and there are several areas we are monitoring closely as we move into 2026.

Our 2026 Outlook

-

If interest rates continue to decline in 2026, we believe this could create a more supportive environment for small‑cap companies. Lower borrowing costs tend to benefit smaller businesses more than large multinational companies because they rely more heavily on affordable financing to grow.

For this reason, we are actively exploring whether to introduce a carefully sized allocation to small‑caps within our Medium and Upper Medium risk portfolios in future. This would not be a short‑term trade - rather, it would be a strategic shift to capture an emerging long‑term opportunity, but only if conditions continue to improve.

-

Global demand for rare earth metals and critical minerals is increasing due to their essential role in technology, electric vehicles, batteries, defence systems, and renewable energy supply chains.

We are currently reviewing ETFs that provide diversified exposure to companies involved in rare earth extraction and processing. This theme is aligned with long‑term structural trends rather than short‑term speculation, and adding it in future may enhance diversification while capturing an important global growth area.

-

There has been growing speculation that Kevin Hassett, President Trump’s top economic adviser and former Chair of the Council of Economic Advisers, could be appointed as the next Federal Reserve Chair, with a decision expected later in 2026 as Jerome Powell’s term expires in May. While no final decision has been made, Hassett is widely viewed as one of the leading contenders. [cnbc.com], [politico.com]

Hassett has repeatedly stated that the Federal Reserve is “way behind the curve” on lowering interest rates and has argued that the U.S. should be cutting more aggressively. In interviews, he has highlighted that strong growth alongside falling inflation gives the Fed “plenty of room to cut rates” and that he would support significantly lower interest rates if he were in charge.

Markets Expect Him to Be Dovish

Analysts and financial media describe Hassett as firmly pro‑growth and likely to support a much more accommodative policy stance than Powell. Reports indicate he has previously suggested he would pursue larger rate cuts, even 50‑basis‑point moves, if needed. His philosophy aligns with the White House’s preference for materially lower interest rates.

A Fed Chair inclined to cut rates more aggressively typically supports:

· Equities, especially growth and technology stocks

· Credit markets, as borrowing costs fall

· Small‑cap and cyclicals, which benefit more from lower rates

· Global risk sentiment, given lower dollar funding costs

A Note of Caution - Nothing Has Been Decided Yet

While Hassett has been viewed as a frontrunner, President Trump recently signalled some hesitation, and other candidates remain under consideration. Political dynamics, ongoing investigations into Powell’s earlier testimony, and internal White House debates mean that the situation is still evolving. Multiple reports confirm that a decision has not yet been made, and markets will likely need to wait until later this year to know who will replace Jerome Powell.

While all of these opportunities are promising, none of them justify immediate changes to portfolio positioning. Any adjustments must:

Improve long‑term outcomes

Maintain liquidity

Preserve diversification

Fit within our disciplined investment process

For now, the best course of action is to stay patient and avoid short‑term thinking. We will revisit each of these potential enhancements as conditions evolve and will only implement them when it is clearly in clients’ long‑term interests.

Key Takeaways

-

Maintaining long-term discipline continues to reward investors.

-

Our portfolios remain balanced and aligned with each client’s objectives.

-

Inflation is easing, and markets are adjusting to a new normal of moderate growth and stable returns.

-

We continue to monitor opportunities for rebalancing as interest rate expectations evolve.

This report is provided for information purposes only and does not constitute personal investment advice. The content reflects Welsh & Taylor Wealth’s views as at January 2026 and may change without notice.

Past performance is not a reliable indicator of future results. The value of investments and the income from them can fall as well as rise, and you may not get back the amount originally invested.

All investments carry risk. The portfolios described in this document are subject to market risk, currency risk, and, in some cases, liquidity and credit risk. Diversification does not guarantee a profit or protect against loss in a declining market.

Tax treatment depends on individual circumstances and may change in future. If you are unsure about the suitability of any investment, you should seek personal advice.

Welsh & Taylor Wealth is a trading name of WTW Ltd, which is authorised and regulated by the Financial Conduct Authority (FCA).