Market & Portfolio Update

Q1 2026

Prepared by the Investment Management Committee – April 2026

This report is provided for information purposes only and does not constitute personal investment advice. The content reflects Welsh & Taylor Wealth’s views as at April 2026 and may change without notice.

Market Overview

Q1 2026 has been one of the most volatile quarters in recent years. Markets entered the year with optimism about cooling inflation and anticipated interest rate cuts across the US, UK, and Europe. However, geopolitical tensions in the Middle East, particularly involving Iran, triggered a sharp surge in energy prices, reshaping global expectations.

For the UK and Europe, the impact has been especially pronounced. Both regions are major net importers of energy, meaning higher oil prices feed directly into inflation, industrial costs, and consumer spending. This creates a stronger economic headwind than in the US, where domestic production reduces exposure to global oil shocks.

Despite this, several sectors within the UK and Europe tend to show resilience during periods of elevated energy prices:

Pharmaceuticals & Healthcare – stable demand

Consumer Staples – non cyclical consumption

Utilities & Infrastructure – regulated pricing

Value oriented equities – financials, telecoms, industrials

High quality dividend payers – strong balance sheets

These sectors continue to provide stability even when headline markets come under pressure.

The Strategic Importance of the Strait of Hormuz

The Strait of Hormuz is the most strategically critical energy chokepoint in the world. It serves as the primary maritime route for Middle Eastern oil exports and is bordered by Iran to the north and Oman/UAE to the south.

How much energy flows through it?

In 2025, the Strait carried - 20 million barrels of oil per day, equating to 20% of global petroleum liquids consumption and 25% of the world’s seaborne oil trade.

It is also responsible for 19–20% of global LNG exports, primarily from Qatar and the UAE.

Since the conflict intensified: Daily tanker transits have collapsed by 90–95%, as vessels avoid the high risk of drone and missile strikes.

Outbound shipments from the Persian Gulf fell to near zero in late February and March.

Major producers such as Saudi Arabia, Kuwait, and Iraq cut output because they could not load crude onto tankers due to full storage.

This makes the Strait of Hormuz effectively the jugular vein of the global energy system, where any disruption instantly impacts global oil prices, shipping costs, and inflation expectations.

Why Iran sees the Strait as key leverage

Most regional producers (Iraq, Kuwait, Qatar, Bahrain, and Iran itself) rely almost entirely on the Strait for exports.

Iran’s geographic position allows it to threaten shipping and control chokepoint access.

As long as tensions persist, oil markets will remain highly sensitive to any developments in the region.

Market Volatility

The primary driver of Q1’s volatility was “super concentration”. Which is a period where a single global variable dominates all markets.

The chain reaction:

Oil rises → Inflation expectations rise → Interest‑rate cuts become less likely → The US dollar strengthens → Gold, equities, and bonds all come under pressure.

The strength of the US dollar was particularly impactful. A stronger dollar typically causes:

Gold prices to fall, even in periods of geopolitical tension

Emerging markets to weaken

Global equities to struggle

Non‑US commodities to decline

This is why portfolios saw correlated weakness across many asset classes simultaneously.

Could Markets Fall Further?

One of the most common investor questions this quarter has been:

“Is this the bottom?”

The honest answer is: we don’t know for sure and neither does anyone else.

“Could markets fall further?”

Yes. The volatility triggered by the Iran conflict and oil market disruption may continue.

But context matters: Since Russia invaded Ukraine on 24th February 2022, the MSCI World Index is still up +58.41%.

Even after this quarter’s pullback, long‑term investors remain significantly ahead. Market bottoms are only visible in hindsight. Attempting to time them introduces more risk than reward.

Central Banks: Rate Cuts Now Less Likely

At the start of the year, markets expected multiple 2026 rate cuts. The rise in energy costs has made that far less likely.

Energy‑driven inflation does not respond well to interest‑rate policy.

Central banks cannot cut aggressively while inflation expectations remain elevated.

However, rates also cannot rise too sharply without risking recession—unlike 2022, when starting rates were near zero.

We expect:

A longer period of restrictive policy, not tightening

Cautious central bank communication

Gradual adjustments based strictly on data

Portfolio Insights

Our investment committee regularly reviews portfolio positioning to ensure alignment with market conditions, long-term strategy, and client outcomes.

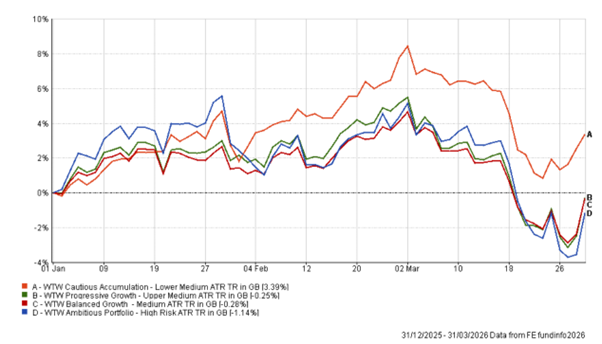

Portfolio Performance in Q1 2026 (1 January – 31 March)

WTW Ambitious Accumulation: -1.14%

WTW Progressive Growth: -0.25%

WTW Balanced Growth: -0.28%

WTW Cautious Accumulation: +3.39%

Q4 2025 Portfolio Performance (1 January 2026 – 31 March 2026)

Assessing Value and Client Outcomes

As part of our ongoing commitment to delivering good outcomes for clients, we regularly assess whether our portfolios continue to meet their stated objectives and represent fair value. This involves reviewing performance, cost efficiency, risk management, and suitability against client expectations and the broader market environment.

-

Risk Profile: Lower Medium

Total Return: +3.39%

Sharpe Ratio: 1.13

Annual Fund Charge: 0.17%

Objective:

To achieve long-term growth while managing volatility through diversification across fixed interest, cash, commodities, and equities. This balanced approach allows access to growth markets while reducing exposure to the fluctuations of the overall stock market.Assessment:

The Cautious Portfolio has delivered +10.86% since launch (8 July to 31 March 2026), which we consider a strong outcome given its defensive positioning and low risk exposure. The portfolio has benefited from steady bond and money market performance, alongside modest equity growth and positive contributions from gold.Volatility remains low and within the portfolio’s target range.

Diversification is delivering as intended — smoothing returns through a mix of defensive and growth assets.

Ongoing charges remain competitive relative to the peer group, and the fund mix continues to prioritise liquidity and cost efficiency.

Overall, the portfolio is meeting its objective of steady growth with controlled risk, representing fair value for investors seeking capital preservation and gradual appreciation.

-

Risk Profile: Medium

Total Return: -0.28%

Sharpe Ratio: 1.24

Annual Fund Charge: 0.09%

Objective:

To provide long-term capital growth by investing across developed global markets. The portfolio balances growth opportunities with risk management, aiming to deliver strong returns over the medium to long term.Assessment:

Since launch, the Balanced Growth Portfolio has returned +10.93%, reflecting strong global equity performance alongside well-managed fixed income exposure.The portfolio’s equity exposure has captured global market gains, particularly from US and developed world indices.

Diversified bond holdings have provided stability and income.

Risk-adjusted performance (Sharpe ratio of 1.35) indicates efficient returns relative to volatility.

The portfolio continues to offer fair value, achieving solid growth while keeping volatility at an appropriate level for investors with a balanced risk appetite.

-

Risk Profile: Upper-Medium

Total Return: -0.25%

Sharpe Ratio: 1.18

Annual Fund Charge: 0.07%

WTW Progressive Growth Portfolio

Objective:

To generate long-term capital growth by providing broad exposure to global equity markets. With an allocation of 80–100% in equities, the portfolio seeks to benefit from growth opportunities across developed and emerging markets while maintaining diversification.Assessment:

The Progressive Growth Portfolio has achieved +13.34% since launch, driven by strong US equity exposure and contributions from global developed markets.The portfolio is performing in line with expectations for its risk level.

Returns have been achieved with controlled drawdowns and strong diversification.

Fees remain competitive compared to similar actively managed portfolios, supporting positive long-term value.

The Progressive Growth Portfolio is delivering on its goal of high-conviction, diversified global growth, and continues to represent fair value by balancing cost, performance, and risk effectively.

-

Risk Profile: Upper Medium

Total Return: -1.14%

Sharpe Ratio: 1.45

Annual Fund Charge: 0.20%

Objective:

The WTW Ambitious Growth Portfolio is designed to deliver high long-term capital growth by investing with a high-conviction, globally diversified equity strategy. With an allocation of 90–100% in growth-oriented equities and commodities, the portfolio focuses on powerful structural growth themes - including global technology leadership, small-cap innovation, and selective emerging-market exposure - while maintaining diversification across regions and asset classes. The portfolio aims to capture the strongest long-term return opportunities available in global markets, accepting a higher level of volatility in pursuit of superior capital appreciation.Assessment:

Since launch, the Ambitious Growth Portfolio has achieved +13.98%. This strong result has been driven by several key factors:High-conviction exposure to the NASDAQ 100 (60%), which delivered robust multi-period returns driven by global technology leaders.

Positive contribution from global small caps, supporting diversification across market cycles.

Strong performance from physical gold (+50.58% over the past year), providing both growth and downside protection in a volatile macro environment.

Selective emerging-market exposure, particularly China, adding a differentiated return stream.

Risk-adjusted metrics remain strong for a high-growth strategy, with the portfolio delivering a Sharpe ratio of 1.45, reflecting efficient capture of global equity returns relative to volatility. The portfolio has demonstrated controlled drawdowns relative to its growth target, with performance remaining within expectations for a high-risk mandate.

Summary:

Across all three portfolios, performance has been positive and risk levels are consistent with client expectations and the stated aims of each strategy. The combination of robust investment governance, transparent costs, and strong early performance indicates that the WTW portfolio range is delivering good outcomes and represents fair value for clients

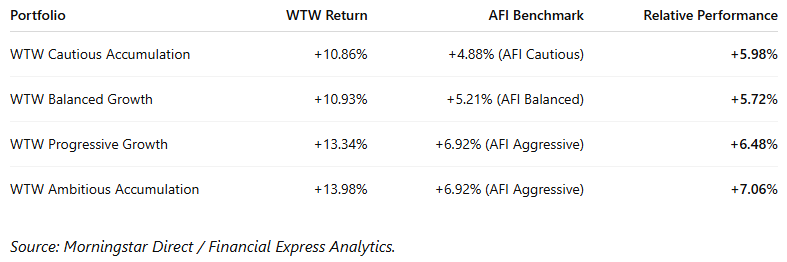

How Do Our Portfolios Compare?

To assess performance objectively, we compare our portfolios against the Adviser Fund Index (AFI) - a recognised industry benchmark compiled by Financial Express from the recommended portfolios of leading UK financial advisers.

The AFI represents a realistic “market average” for professionally managed portfolios across three risk levels:

AFI Cautious - lower-risk portfolios with a higher allocation to bonds and cash.

AFI Balanced - medium-risk portfolios combining equities and fixed income for steady growth.

AFI Aggressive - higher-risk portfolios with greater exposure to global equities.

By comparing each WTW portfolio to its corresponding AFI benchmark, we can objectively determine whether our portfolios are providing clients with added value relative to the broader advice market.

Performance Comparison (8 July 2025 - 31 March 2026)

Why Our Portfolios Have Outperformed

Our portfolios have delivered stronger returns than their respective AFI benchmarks for four clear and consistent reasons. These advantages apply across the full Welsh & Taylor Wealth range - Cautious, Balanced, Progressive, and Ambitious - and reflect our disciplined, evidence‑based investment approach.

-

Many UK‑advised portfolios retain a strong domestic bias, often overweight in:

UK equities

UK gilts

UK corporate bonds

While parts of the UK market performed well at points over the past year, the strongest long‑term, risk‑adjusted opportunities have continued to come from global markets, particularly:

US large‑cap equities (S&P 500 strength)

Developed world markets

Technology leadership in the US and Asia

European equity resilience

Global small caps (Ambitious portfolio)

Selective exposure to China (Ambitious portfolio)

Because our portfolios are intentionally built with broad, global exposure, they have benefited directly from:

Strong returns across the S&P 500

Robust performance in developed world indices such as MSCI World

Positive relative performance in Europe

High‑growth sectors that UK‑centric portfolios typically underweight

This global orientation helped lift returns and provided more diversified participation across economic cycles, especially compared to UK‑focused AFI benchmarks.

-

Gold has been one of the standout diversifying assets over the period under review. Our decision to include a deliberate 10–15% strategic allocation to physical gold has added meaningful value across all four portfolios.

Gold supported performance because:

✅ Geopolitical uncertainty increased safe‑haven demand

With rising global tensions, energy market instability, and uncertainty across major regions, gold continued to act as a store of value.

✅ Expectations of long‑term rate cuts strengthen gold’s appeal

As inflation stabilises and long‑term monetary easing becomes more likely, the opportunity cost of holding gold falls - historically a supportive environment.

✅ Central banks continue to favour gold over the US dollar

Long‑term structural buying from global central banks reinforces gold’s importance as a reserve asset.

✅ AFI benchmarks have little or no gold exposure

This has created a significant performance gap:

When gold rose, WTW portfolios benefited

When equities wobbled, gold provided ballast

When bonds struggled, gold offered non‑correlated support

Gold’s dual role - return enhancer and volatility dampener - has been a key driver of our outperformance.

-

All WTW portfolios use:

✅ Institutional‑class passive index funds

✅ Highly liquid ETFs

✅ Low‑cost, transparent holdings

✅ No high‑fee active managementLower costs mean:

Clients keep more of their returns

Performance reflects markets cleanly, without unnecessary fee drag

Rebalancing is efficient and friction‑free

There is no manager‑specific risk, style drift, or concentrated exposure

By contrast, many portfolios represented in the AFI benchmarks rely on:

Higher‑cost active funds

Less liquid or less efficient structures

Significant fee drag and turnover costs

Our cost‑efficient implementation is a systematic and persistent source of outperformance.

-

Critically, our stronger returns did not come from taking more risk. In fact:

✅ All four portfolios showed:

Higher Sharpe ratios than their AFI equivalents

Positive alpha relative to benchmarks

Better downside protection during volatile periods

This demonstrates that outperformance came from:

Diversification

Intelligent asset allocation

Gold exposure

Global market participation

Lower costs

Disciplined long‑term positioning

Not from concentration or excessive risk‑taking.

outcomes over time.

We remain confident that this approach will continue to add value as markets evolve into 2026.

Our Philosophy

At Welsh & Taylor Wealth, our investment philosophy is built around a simple but powerful truth:

“You can behave like a trader… or behave like an investor.”

We choose, deliberately and consistently, to be investors. In volatile periods like Q1 2026, the difference becomes even more important.

Traders vs Investors

-

Traders try to predict short‑term movements. Their mindset is often driven by:

reacting to headlines

guessing market direction

moving in and out quickly

timing peaks and troughs

responding emotionally to volatility

This approach feels exciting, but it relies heavily on speculation and luck, especially during geopolitical events or energy‑driven markets where information is incomplete, unreliable, or quickly outdated. In practice:

❌ Traders are often right too early or wrong too late

❌ Short‑term market moves are unpredictable

❌ Emotional reactions lead to poor outcomes

❌ Timing mistakes compound faster than returnsEven professionals find it extremely difficult to consistently profit from short‑term moves and that’s in calm markets, not quarters like this one.

-

Investors, especially long‑term macro investors like us, approach the market fundamentally differently.

We focus on:

✅ Long‑term economic trends

✅ Diversification across global markets

✅ Fundamentals, not headlines

✅ Costs, liquidity, and risk management

✅ Repeatable and disciplined process

✅ Staying invested to capture compoundingWe know volatility is not the enemy. In fact, it’s: “The price of admission for long‑term returns.”

Our clients understand that portfolios grow over years and decades - not hours or days.

This philosophy is built on evidence:

Markets reward patience

Diversification reduces long‑term risk

Lower costs improve net returns

Time in the market matters far more than timing the market

Being an investor means embracing temporary discomfort to achieve permanent progress.

We Are Macro Investors Using Passive Instruments

This is a key part of our identity, and something clients find helpful when it’s clearly explained.

✅ What does “macro” mean?

We analyse global forces that drive markets, such as:

Inflation

Energy prices

Interest‑rate policy

Demographics

Productivity

Long‑term trends across regions and sectors

We are not stock pickers.

We are not trying to outguess markets at the company level.

We focus on the broader global environment and choose asset classes, regions, and factors that align with long‑term structural trends.

Why do we use passive instruments (ETFs & index funds)?

Because passive, index‑based approaches:

Keep costs low

Keep liquidity high

Avoid manager risk

Reduce behavioural errors

Capture long‑term market growth efficiently

Passive instruments allow us to express macro views without trying to hand‑pick winners.

For example:

Instead of choosing which tech company may outperform, we allocate to a broad global tech index or developed world index.

Instead of picking a single pharmaceutical stock, we hold diversified healthcare exposure.

It is disciplined.

It is scalable.

It is evidence‑based.

It is transparent.

Clients can clearly see what they own, why they own it, and how it fits their long‑term strategy.

Why We Are Not Making Any Changes at This Time

As we progress through 2026, our core message remains straightforward: we are not making any changes to the portfolios at this time. Each of our strategies continues to behave exactly as intended - balancing growth, risk, diversification, and liquidity in a consistent and repeatable manner.

-

Recent geopolitical tensions - particularly those involving the Middle East and the disruption to energy markets - have created an environment where information is inconsistent, fast‑moving, and often unreliable.

This is especially true for news flow coming out of Washington and Tehran, where statements, interpretations, and updates frequently conflict. In situations like this, attempting to trade tactically on every headline is not a disciplined investment strategy - it is speculation.

✅ When you cannot trust the information,

✅ and you cannot predict the outcome,

✅ the most rational action is often to take no action at all.

Over‑trading in volatile environments is one of the fastest ways to destroy long‑term returns. Markets can move sharply on rumours and reverse just as quickly when new information contradicts the old. Acting reactively risks locking in unnecessary losses or missing subsequent rebounds.

Sometimes, doing nothing is a decision - and often the correct one.

-

Our portfolios are not designed to chase headlines or react to short‑term geopolitical swings. They are constructed with a clear and disciplined philosophy:

Focus on long‑term outcomes, not short‑term reactions

Accept that volatility is normal and expected

Avoid trying to “predict” fast‑moving geopolitical events

Rely on global diversification, not concentrated bets

Stay consistent with our macro‑driven investment framework

Use high‑quality, low‑cost passive instruments

This architecture is precisely why our portfolios have delivered such strong risk‑adjusted results since launch. We do not deviate from our process simply because the news cycle feels uncomfortable.

-

Our investment committee continues to monitor:

global interest‑rate policy

inflation trends

energy market dynamics

currency movements

long‑term structural opportunities

But monitoring does not mean reacting.

We will only implement changes when three conditions are met:

The macroeconomic environment genuinely shifts, not just intraday sentiment

The proposed change improves long‑term outcomes, not short‑term optics

The change maintains or enhances diversification, liquidity, and cost efficiency

Until those criteria are satisfied, maintaining current positioning is the most appropriate and disciplined response.

Looking Ahead

While we are not making changes at this time, our forward‑looking research helps identify where long‑term opportunities may arise as conditions evolve.

These are not predictions - they are themes we are monitoring carefully.

Sectors likely to benefit or remain resilient

-

Demand remains stable regardless of economic conditions

Strong pricing power

Defensive qualities

-

Essential goods maintain consumption

Lower volatility

Historically outperform during slowdowns

-

Regulated returns

Often inflation‑linked

Long‑duration cashflows

-

Financials, telecoms, and industrials

Lower sensitivity to high growth expectations

Often cheaper valuations entering slowdowns

-

Strong balance sheets

Reliable cashflow

More defensive behaviour

We are evaluating whether any of these areas warrant future inclusion or adjustment if macro conditions evolve toward stagflation risk.

Technology: Now Looking More Attractive

Technology was one of the hardest‑hit sectors in Q1, but that downturn has created more reasonable valuations.

A stark example:

Nvidia’s price/earnings ratio is now comparable to ExxonMobil’s.

This was unthinkable 12 months ago.

It does not automatically mean “buy now,” but it signals a shift:

✅ The extreme valuations of 2023–2025 have reset

✅ High‑quality tech is now priced more rationally

✅ Future earnings may look more attractive if rates stabilise

We expect tech to remain a major long‑term engine of global growth - but we prefer to enter sectors at sensible valuations, not euphoric ones.

Energy: A Tempting but Dangerous Cycle

Energy stocks have been strong performers this year, but the risks are significant:

Oil prices are being driven by geopolitical scarcity, not steady fundamentals

The sector is extremely volatile

Buying after a spike can lock in losses if conditions normalise

Historically, energy is among the fastest “boom‑to‑bust” sectors globally

As anyone with experience in energy markets knows:

“When it booms, it booms - but when it reverses, it reverses brutally.”

For now, energy remains a high‑risk, high‑volatility proposition. We are monitoring it, but not allocating heavily at elevated prices.

Rare Earths & Critical Minerals

Long‑term demand continues to rise due to:

Electric vehicles

Battery technology

Defence systems

Renewable energy

Semiconductor production

We are reviewing diversified ETF solutions that could provide:

global exposure

reduced single‑country risk

long‑term structural growth potential

This theme remains on our radar for potential strategic inclusion.

Fixed‑Income Opportunities

If inflation stabilises and the path for rate cuts clears, we may explore:

Extending bond duration

Adding more high‑quality corporate exposure

Selectively increasing global sovereigns

But we will only do this when the macro data genuinely supports it.

Key Takeaways

-

Long‑term discipline continues to be the most reliable driver of returns.

Even in a year marked by geopolitical tension, energy shocks, and fast‑moving headlines, patient investors have been rewarded. -

Our portfolios remain well‑diversified and aligned to each client’s long‑term goals.

This includes exposure across global markets, sectors, and asset classes, supported by a macro‑driven, passive approach. -

Markets are adjusting to a more stable inflation environment and a slower, more data‑dependent interest‑rate cycle.

Volatility may persist, but the underlying trends remain constructive for long‑term investors. -

We continue to monitor opportunities carefully - but we will only rebalance when it supports long‑term outcomes.

In periods where the outlook is unclear, doing nothing is often the most disciplined and effective action.

This report is provided for information purposes only and does not constitute personal investment advice. The content reflects Welsh & Taylor Wealth’s views as at April 2026 and may change without notice.

Past performance is not a reliable indicator of future results. The value of investments and the income from them can fall as well as rise, and you may not get back the amount originally invested.

All investments carry risk. The portfolios described in this document are subject to market risk, currency risk, and, in some cases, liquidity and credit risk. Diversification does not guarantee a profit or protect against loss in a declining market.

Tax treatment depends on individual circumstances and may change in future. If you are unsure about the suitability of any investment, you should seek personal advice.

Welsh & Taylor Wealth is a trading name of WTW Ltd, which is authorised and regulated by the Financial Conduct Authority (FCA).